What Happens When a European Stock Broker Goes Bust?

No one ever expects their stock broker to go bankrupt, but it’s a real possibility. If your broker goes under, what happens to your investments? Will you lose everything? It’s unlikely, but here’s what you need to know as a European investor to protect yourself.

What happens if my stock broker goes bankrupt? Are my shares and cash deposits gone forever if the broker shuts its doors? These are questions that have been addressed many times before, but they remain a mystery to most.

Many investors are unaware of how their shares are held and the risks to their accounts if things go south. In this article, we’ll discuss how European online brokerages work and what exactly happens in the event of a bankruptcy.

Here’s a summary of the key takeaways

- Broker bankruptcy is uncommon but can happen. If a broker goes bust, your equity (shares and ETFs) will be transferred to another broker and be safe. However, there are risks associated with this process.

- It’s your stock, just not in your name. When you buy stocks, they’re usually registered in the name of your broker rather than under your name. This is known as omnibus or street name registration. The brokerage firm is the legal owner of the shares, but you are the ultimate beneficiary.

- In the event of bankruptcy, administrators compare the internal records of the defaulted broker with the records of the securities depository where ownership is registered. If there are no discrepancies, investors will not be affected.

- Asset segregation is the strongest firewall for investors. Segregation ensures that your cash and stocks are separated from the brokerage firm’s own assets.

- Fraud is not common, but poor recorded keeping is. Even if you have a reputable broker regulated by prominent financial authorities, it’s still important to keep track of accounts. Good documentation may be one of the most effective methods to demonstrate ownership of your assets.

- Investor compensation schemes are a last resort. If the broker engages in fraudulent activity or has errors in its internal ownership records, only then would investor compensation schemes become relevant. If this happens, investors will be compensated for a loss of between 20,000 and 100,000 EUR, depending on the jurisdiction of the broker.

- Securities lending is muddy waters. It’s increasingly common for brokers to lend out their customers’ stocks to generate income. While borrowers provide collateral in excess of the value of the stock loaned, there is always a risk that the borrower is unable to repay the loan if the markets rally. While the risk is minor, this could impact investors during a broker’s bankruptcy.

Trust a stranger with your money?

Here’s an interesting thought: Why not transfer thousands of euros, pounds, or dollars to a company you’ve never visited or just heard of last month and trust that they’ll hold onto it for you? Seems a bit risky, right?

This is what investors do on a daily basis when they participate in the stock market. They entrust their money to a company on the internet and assume that their money is in good hands.

They never met the people behind the company. They have no idea what their office looks like. Yet, they’re happy to transfer them enormous sums of money, click that mouse button, and assume their broker purchases and secures their shares for them.

This would be complete lunacy if it weren’t for the fact that there’s a robust regulatory framework in place to protect investors. The most important aspect of this framework is asset segregation.

Asset segregation: A core principle

Asset segregation means that broker must separate customer funds from its company assets. The separation of company assets from customer assets ensures that investors are not held responsible for the firm’s debt in case of bankruptcy. Any creditor claims against the firm are paid from the company’s own assets, not from customer funds.

All licensed securities account providers in the EU, UK, U.S., and other major economies must maintain segregation. Taking the EU as an example, the segregation of client assets falls under various regulations, including AIFMD, EMIR, CSDR, UCITS V, and MiFID/MiFIR. These regulatory frameworks are designed to protect investors, and as a result, ensure the safety and soundness of the financial system.

What exactly is meant by asset segregation?

When it comes to segregated accounts, two types of accounts are important to understand: internal and external.

Internal accounts are those that are recorded on the books of the securities account provider, and they reflect the holdings that the clients have with that provider.

You can think of the internal account as a giant electronic ledger where every transaction and balance is recorded. This is like the accounting program you would use for your company; it’s just much more sophisticated.

- A securities account provider must maintain at least one internal account for each client, identifying the client in relation to their assets.

- On the basis of a request from the securities account holder, the internal accounts will also show whether the assets contained in that securities account are owned by the account holder or whether the brokerage is holding them on behalf of their clients.

External accounts are the accounts opened by the securities account provider at a third party to hold client assets. Remember that securities are not registered with the broker itself but with a securities depository, custodian bank or clearinghouse. These external accounts are typically operated by large and well-known institutions such as Euroclear (Belgium), Clearstream (Luxembourg), and DTCC (U.S.).

- The provider of the securities account (i.e., the broker) will separate its own and customer assets when opening the external account with the depository or other third party. If the brokerage uses omnibus accounts (see below), the account will be in the broker’s name. Still, it will make it clear that the client of the broker is the ultimate owner.

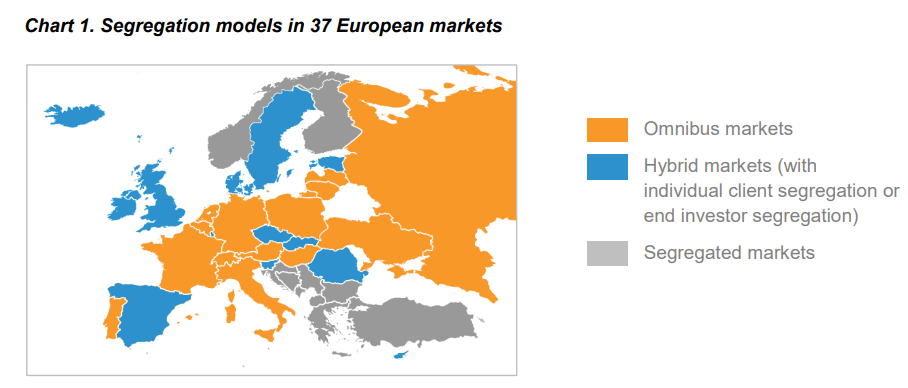

- Most European securities account providers use omnibus accounts, which consolidate the assets of a financial institution’s clients into a single external account. In some markets, however, identification of the ultimate beneficial owner of assets is required. A separate external account will be opened for each client of the securities account provider. This is known as direct-holding or direct registration.

- Although the rules are closely harmonized, their implementation may vary. Certain European jurisdictions require the broker to maintain separate external accounts for each client.

Here’s an overview of the different segregation models are used in Europe:

The distinction between internal and external accounts is essential when determining what happens to client assets in the event of a broker going bankrupt. Suppose the broker doesn’t keep proper internal accounts. In that case, the insolvency administrators may not be able to tell which assets are client money and which belong to the broker. In this case, all assets in external accounts could be hard to identify.

How cash deposits are protected

The first step is when you transfer money from your bank account to your broker. This is the liquidity you will use to buy stocks, ETFs, or other financial instruments.

As long as your money sits in your own bank account in the EU, it’s protected up to €100,000 (or equivalent amount in the local currency). This amount is universally guaranteed across all Member States in the European Union. All licensed banks must contribute to a Deposit Guarantee Scheme (DGS) that reimburses depositors in the event of a bank failure.

In the UK, a similar compensation scheme guarantees deposits of up to £85,000. In Switzerland, the depositors’ insurance fund insures deposits of up to CHF 100,000. So the list goes on for other countries.

Once your money lands in your brokerage account, the protection looks a little different depending on whether the broker is a licensed bank or not.

Cash segregation

MiFID (the holy grail of European financial regulation) demands that broker account provider firms separate cash from their own assets (through the omnibus model) with third-party banks or in qualifying money market funds. Bank-licensed brokerage firms are required to follow the same rule, but they use the direct separation model to separate each client from other clients (meaning, no omnibus pooling) and the bank of the brokerage itself.

Brokers with a banking license

If the broker has a banking license, it’s subject to the same rules and regulations as any other bank. Your uninvested cash is protected up to €100,000 per account holder, just as if it was in your bank account. If the broker goes bankrupt, your cash deposits are guaranteed by the state where the broker is registered. If you have a joint account, e.g., with your partner, you’re collectively covered for up to €200,000.

The responsible national deposit guarantee fund must repay your deposits within 7 working days. The compensation will be sent to another bank where you have an account so that you can access the funds as soon as possible.

Personal bank account

Suppose your broker is located in the EU and has a banking license. In that case, there’s a very high chance that you will have a personal IBAN (International Bank Account Number) and BIC (Bank Identifier Code) as well. Funds in this account will be held in your name and not the name of your broker. But it’s unlikely that it will have the same functionality as your bank account, so it’s best to think of it as a holding account.

Brokers without a banking license

Brokers without a banking license must still comply with stringent rules and regulations regarding asset segregation. However, they’re not regulated as banks, and your cash deposits are therefore not as well protected.

Let’s start by looking at what happens when you put money into a brokerage that isn’t regulated as a bank.

Pooled bank accounts

When you want to deposit money into your brokerage account, you usually have to send it to a bank account held in the name of your broker. You’ll be asked to provide your name and a number as a reference so the transaction can be linked to your account. This means that you’re now transferring the money to an account owned by the broker and not yourself.

This is important because your funds are now pooled in the broker’s bank account with hundreds or thousands of other clients. A bad broker will have 100% exposure to that single bank account and not spread the deposits over multiple banks. Suppose that a single bank goes out of business. In that case, your money is at risk because you are not the account owner and the deposit guarantee only covers individual bank accounts.

Conduit accounts

A good broker will not keep all of the funds in one bank account but instead distribute them across several large (“too big to fail”) banks. It uses the receiving account as a conduit account, as an entry and exit point, to spread customers’ funds across several other institutions. This way, the risk exposure to each individual bank is lowered accordingly.

Money market funds

A non-bank broker has the right to keep your cash in money market funds, which are usually considered safer than omnibus bank deposits. A money market fund is a type of mutual fund that invests in short-term debt securities, such as certificates of deposit (CDs), commercial paper, and government bonds.

Money market funds are typically managed by large banking corporations, and are considered a safe investment, and are rated 1 (lowest) on a scale from 1 to 7. However, they are not protected by the deposit guarantee scheme. Despite the lack of official state protection, money market funds are considered a much safer place to park large sums of money than pooled bank accounts. Around €1 trillion of European cash is invested in money market funds.

While money market funds are generally considered safe, they are not risk-free.

What to look for

If your broker doesn’t have its own banking license, it’s not only essential to make sure that customers’ deposits are spread across several banks. It’s equally important that these banks are considered “safe havens.”

You don’t want your money to be trapped with thousands of other customers in a tiny national bank that is entirely dependent on the local market’s political or economic atmosphere. A globally operating mega-bank subject to international supervision from multiple independent financial authorities should always be the first choice.

Cash protection in brokerage accounts – does it really matter?

Many investors use the same argument when it comes to cash protection in brokerage accounts: “I don’t keep any cash there, so I’m not concerned.” However, many investors actually park their funds in the account to buy or sell stocks quickly when opportunities arise. Another reason may be that they use the account to avoid paying negative interest rates charged by their bank. Many investors who have more than average cash balances also use currency accounts to protect themselves against unfavorable changes in foreign exchange rates.

The bottom line is that, while your shares might be safe in the event of a broker bankruptcy, your cash deposits are only as safe as the bank that the broker uses to store them.

How shares are protected against broker bankruptcy

The principle of asset segregation is a crucial pillar of the investment industry. Segregation ensures that client assets are kept separate from the broker’s company funds and out of the hands of creditors during insolvency proceedings.

The fundamental objective of asset segregation is to guarantee that the assets of the customer are not included in the bankruptcy estate of the broker. Asset segregation also protects against the mingling of customer and broker’s assets and from unauthorized use by the broker.

Understand these three ways to hold shares

You’ve undoubtedly come across discussions about direct registration vs. street-name registration when looking online. In a European context, direct and street name registration are not proper legal terms but Americanisms that have found their way across the pond.

There are, correctly speaking, two different types of segregated accounts – Individual Segregated Client Accounts (“ISA”) and Omnibus Segregated Accounts (“OSA”).

An ISA will contain the assets of just one client, whereas an OSA will hold the assets of several clients.

When you hold securities as a private investor, there are three ways to do it: through a physical paper certificate, electronic form with direct registration, or in electronic form in nominee accounts.

- Physical stock certificates. The traditional way of holding stocks directly is with a paper certificate. You would receive this physical document confirming your ownership and appear on the register as a shareholder, except in the case of anonymous bearer certificates. If you inherit stocks from your grandmother, they are likely in physical form. The practice of issuing physical ownership certificates has largely vanished with the introduction of electronic registration.

- Electronic direct registration. A more modern way to hold stocks is through direct registration. In this case, your brokerage firm is the intermediary between you and the company. Your company stock ownership is recorded electronically in a database at a securities depository. You would be able to receive confirmation of this ownership in the form of a statement. Your name and the number of shares would appear on the company’s shareholder register.

- Electronic nominee registration (also known as “omnibus”, “pooled”, or “street name” accounts). This is the most common way to hold stocks and other securities today. In a nominee account, your name does not appear on the shareholder register for the company. Instead, the name of the brokerage firm appears as the shareholder. You do not receive a physical certificate, and the securities depository registry does not indicate how many shares you own. The brokerage firm is the legal owner of the shares, but you are the ultimate beneficiary.

Physical stock certificates: Direct holding

Physical stock certificates have been issued since at least 1606 with the emergence of the Dutch East India Company. They’re the first example of a direct holding system in which ownership and settlement were handled face-to-face between the firm and its shareholders or between a buyer and seller of the certificates. The issuer’s register would show investors’ names to verify ownership or use bearer shares, which permitted nameless holding.

There are few benefits to physical certificates when looking at them with modern eyes. The main advantages are that they can be traded without going through a broker. The ownership is not dependent on a third-party system. Bearer shares were handy to preserve privacy. However, physical certificates are seen as an inconvenience and an unsafe medium of storage for the most part. They can be easily forged, lost, and/or damaged, they require special handling and storage. They’re paper, after all.

Electronic direct registration

Since the 1960s, holding shares directly has gradually been phased out. The catalyst was the surge in trading activity after World War II and the introduction of computerized transaction recording and processing. This made it possible to complete transactions on a company-by-company basis and for securities depositories to link databases and centralize the tracking of stock ownership.

Central securities depositories (CSDs) emerged in the U.S., the UK, and other developed markets. Securities depositories would gradually hold all publicly traded assets, to be accessed by the issuer, broker, and investor. These entities also provided a safekeeping service for securities. They facilitated the exchange of information between companies, their registrars, and investors. CSDs also enabled the development of registries that showed the ownership of shares.

In an electronic direct registration system, the investor’s name is recorded in the company’s register and/or in the registry of a CSD. Say you buy shares in Microsoft. The shares will be registered in your name at the CSD, and you’ll receive a statement as proof. You don’t actually get physical certificates, but the company’s shareholder register will show that you own shares.

Electronic nominee registration: Omnibus holding

In most countries, having your own name recorded at the central securities depository is unusual these days. Instead, most brokers keep shares of purchases by their clients in so-called omnibus accounts (in the U.S., these equities are usually called “held in nominee” or “held in street name.”).

An omnibus account is a nominee account in which the beneficial owner is not named on the shareholder register. Instead, the name of the brokerage firm appears as the shareholder. The brokerage firm is the legal owner of the shares, but you are the ultimate beneficiary.

It’s entirely legal for stock brokers to hold shares on behalf of their clients in this way, and it’s by far the most common form of share ownership. You might even say that the European Union encourages omnibus holding with its efficient market policy. And omnibus accounts are the most popular registration method among stock brokers because they cut down on expenses while also improving trading efficiency.

If you purchase shares in Microsoft this way, Microsoft won’t know that you hold stock in their company. It won’t see your name on the register of shareholders. Microsoft only sees the name of whatever brokerage firm you bought the shares from. The brokerage firm will have a list of their own Microsoft stock clients, but your name won’t be on any Microsoft shareholder list.

Direct registration vs. omnibus registration: Which is safer?

Let’s repeat the differences between direct and omnibus registration.

In a direct registration system, the investor’s name is recorded in the company’s register and/or in the registry of a securities depository. In an omnibus account, the brokerage firm’s name appears as the shareholder. In turn, the investor’s name appears in the internal accounts of the brokerage firm, connecting the two.

If you’re using an online broker, your securities are almost certainly in a pooled account unless you’re sure otherwise. This implies that the legal owner of the shares is your stock broker, and your assets are combined with those of numerous other investors.

The omnibus registration system doesn’t sound too safe, does it? In fact, many people believe that this system exposes investors to a high level of risk. There’s no definitive answer to the question of whether direct or omnibus registration is safer.

Understandably, an investor would prefer for their name and assets to be recorded at a central securities depository rather than just in the internal accounts of a broker. However, direct registration is not an efficient recording method. It can be very costly for companies, and they would pass on the expense to investors. Omnibus registration has (so far) proven to be a secure middle ground between efficiency, cost, and safety.

Segregated accounts (direct-registration)

The idea behind the direct registration of shares is to register the securities in the name of the beneficial owner (the private investor) rather than that of the broker. This means that the owner is registered as the shareholder in the database of the securities depositary (or a central securities depository).

In the event of bankruptcy and liquidation of the broker, an investor would not have to worry about whether the administrator would be able to find their name in the internal records of the brokerage.

Very few online brokerages employ the method of direct registration because it is too expensive and requires a lot of paperwork and administration. There is simply put too many transactions each day for a broker to handle through direct registration.

Omnibus accounts (street-name registration)

As you might have guessed, an omnibus account is one where the securities are registered in the broker’s name rather than the beneficial owner. This is the most common way of holding securities, as it’s much easier administratively.

Securities held in street name provides quicker trading and lower transaction costs. Most investors care about trading costs and don’t pay much attention to the potential risks associated with this type of account. It’s not mandatory to show any kind of disclaimer for this type of account because regulators consider segregated and omnibus accounts equivalent in legal terms.

Don’t be fooled by account segregation

The separation of funds is a trust system in which you have faith that the broker will keep your assets separate from their own. Fortunately, the system does not rely on trust alone. Regulators do spot checks on stock brokers from time to time to verify that the segregation rules are being followed. However, they do not monitor their accounts in real-time.

So the system is not without risk, but it does provide a significant level of protection. During tough times, company owners are known to break the rules to save their business. The most significant danger is if the broker decides to cover their own losses using your money.

Funny accounting practices have a tendency to occur during turmoil, as we saw during the financial crisis. Finances suddenly appear less shaky than they really are, and some companies go as far as to leave out unpalatable details from their accounts.

Securities lending – an added risk

Securities lending is a relatively common practice. Most stock brokers and asset managers lend securities to other market players. The rental income generated can be used to benefit the investor, for example, when the broker waives fees or reduces commissions on trades. With this in mind, it does not surprise that many brokers offer their clients solutions for securities lending programs.

However, there are risks with regard to securities lending transactions due to several reasons: There have been cases in which borrowers have failed to return shares within agreed time periods; they were even declared bankrupt after defaulting on their obligations under these agreements beyond redemption (usually because an underlying position has moved against them). In addition, there is always the risk that the counterparty could become insolvent, leaving the lender with worthless stock.

This is what happened to Lehman Brothers in 2008 when it filed for bankruptcy. The company had made loans worth billions in securities to other financial firms. It could not recover any of these assets when its borrowers went bust.

The fallout from Lehman’s collapse caused disruptions in global markets, as creditors and counterparties around the world started pulling their money out of anything even remotely linked to the now-defunct bank. This created a liquidity crisis that led to frozen credit markets and an increase in borrowing costs worldwide.

Clearly, securities lending can be a risky business – especially if your broker goes bankrupt during a global market meltdown and you find yourself in a situation where your broker cannot pay for the shares it owes other brokers.

What happens if my broker goes bankrupt?

Let’s assume your broker has gone bankrupt overnight, and you’ve just woken up to the wonderful news. What happens now?

- Once the bankruptcy procedure begins, the broker’s assets will be frozen. This means that you won’t be able to make any withdrawals or transfers until further notice.

- Some businesses have been able to sell themselves to prevent bankruptcy. Other firms self-liquidate, and in that case, the national regulator will appoint a trustee to take control of the company and wind it down.

- Once the administrator is appointed, you will receive a letter informing you of the situation and what will happen next. It may also give you instructions on how to claim your assets and tell you what information and documents to gather.

- If no fraud or misconduct has occurred, the regulator and administrator transfer the client account to a different brokerage firm. Customers are informed that their funds have been moved and told what to do next.

- There’s no fixed amount of days or weeks that the whole process will take. It could be a few months or drag on for more than a year. The speed with which customer securities are returned is determined by various circumstances, including the accuracy of brokerage firm records.

- Investor accounts are legally ring-fenced, but if the administrator cannot recoup fees from company assets, they may instead collect them from client assets.

Asset segregation is a key principle in the financial industry for ensuring that clients’ money is protected from the creditor. However, they are not fully protected from the administrators of the estate. Because the process is time-consuming, expensive, and requires multiple levels of approval from bankruptcy courts, costs can quickly run into the millions. The only way to cover these costs is if the administrator can successfully claw money from investors. This isn’t as terrible as it seems. Brokers are subject to capital requirements set by the regulator. These are intended to cover the administration cost of a bankruptcy. But lawyers have a way of spending more money than expected, and the shortfall can easily fall on investors.

How to prepare for broker bankruptcy

Dodging the bullet of a broker bankruptcy is admittedly easier said than done. None of us are oracles, and not even the best regulators can perfectly predict when a financial institution might fail. But there are steps you can take to protect yourself in advance:

- Direct registration is preferable but don’t fret over it. The omnibus-street name registration system is built to handle bankruptcies. It has been fine-tuned intensively after the 2008 financial crisis to protect customers’ assets. Omnibus accounts can even make it easier for authorities to transfer your assets to a new broker in the case of bankruptcy.

- Recording keeping falls on you, the investor. Keeping track of your assets and their movements is always a good idea, but it’s vital in times of tumult. By keeping copies of your holdings and having an up-to-date paper trail of your transactions, you will be better prepared if something happens to your provider.

- Don’t rely too much on the broker’s pooled bank accounts. If your broker doesn’t have a banking license, it’s better to keep your cash in a separate account. This means that, even if the broker goes bankrupt, you’ll still have access to your money.

- Spread your risk. Diversifying your investments is always a good idea, but by spreading your investments across several reputable brokers, you will better protect yourself in the event of bankruptcy.

Final words

No one wants to think about their broker going bankrupt. It’s a stressful, confusing process that can easily lead to financial disaster. But by being aware of the risks and taking some simple precautions, you can minimize the damage and protect yourself and your assets.

Investor protection systems are intelligently designed. Should a broker go bankrupt, the chances of private investors incurring losses are minimal. While these systems are not perfect, and there are still flaws that need to be addressed, they are generally effective at protecting investors’ interests in times of crisis.

It’s unusual for brokers to go bankrupt. However, the growth of neo-brokers is cause for concern. If the market becomes saturated, the weaker players will fail. There’s no guarantee that bigger brokers are better, but choosing a broker with a sustainable business model might not be the worst idea. To summarize, it’s always a good idea to research a broker in-depth before jumping in with both feet.